Cash Flow at Risk (CFaR) for Liability Management

Often the only meaningful quantitative information processed for decision makers is based upon a single historic average of the market element(s) in question - an interest rate, investment growth rate, commodity price, etc. In the tax-exempt capital markets, this tax-exempt or taxable short term rates and the ratio between the two. The resulting elephant in the room is that these assumptions are wrong. And everyone knows they're wrong. The crucial question beyond, "But what can we do about it?" is "How wrong are these assumptions?" This article, in describing Cash Flow at Risk (CFaR), at least partially addresses both of those questions.

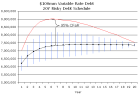

This article details a methodology for calculating CFaR as an alternative to "fixed/floating" mix, explains CFaR's intuitive meaning graphically, and using CFaR compares different financial instrument portfolios through changing market expectations and model assumptions.