SmartModels Utilities: Bootstrap

Everyone in fixed-income has access to certain yield curve analytics. Whether part of a fixed-income pricing system, bond math engine, or a “garage project” spreadsheet, they’re ubiquitous. Our experience is these are either more work or too simple for what's handy day-to-day.

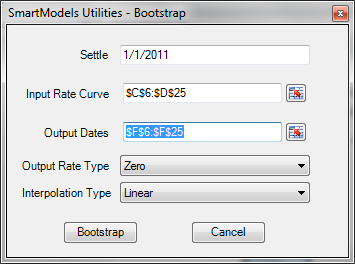

Taking 30/360 semi-annual par yields as input, SmartModels Utilities Bootstrap function gets you to zero, forward, or forward par rates with a click of a button:

- Go to SmartModels Utilities and select Bootstrap from the dropdown

- Enter a settlement date, input curve, and output dates

- Select your output rate type and Linear or Cubic Spline interpolation methods

- Click the Bootstrap button

BENEFITS

- Speed – Delivers just the analysis you need in a quick, easy-to-use interface

- Accuracy – These yield curve analytics are industry standard and thoroughly tested; no spreadsheet formulas to audit

- Speed again - Input ranges are set and stored in the interface until the user changes it, saving additional time when data changes and recalculation is necessary