"Don't ever get your speedometer confused with your clock, like I did once, because the faster you go, the later you think you are." - Jack Handey, Deep Thoughts

"Don't ever get your speedometer confused with your clock, like I did once, because the faster you go, the later you think you are." - Jack Handey, Deep Thoughts

Topics: refunding, advance refunding, negative arbitrage, escrow

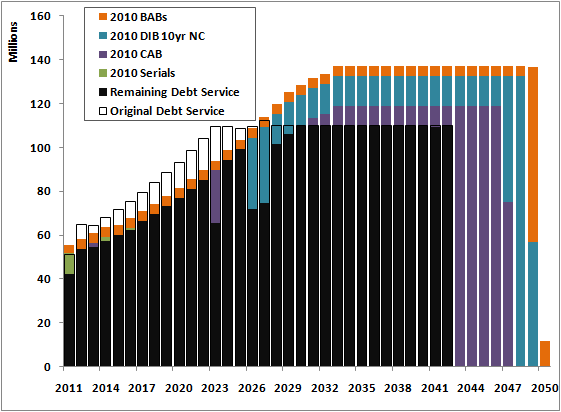

Debt service charts in public finance are as ubiquitous as business cards at a shortlist presentation and date back to before Lotus 123 offered WYSIWYG. Unfortunately, they usually don’t look much different despite just a few improvements in technology over the last 20+ years. But what can you do to make a principal and interest graph sizzle? The answer is *a bunch of stuff* particularly with Excel 2007's new graphics engine. One rule of thumb (and pet peeve of ours): do not ever make your chart in more dimensions than the data. Debt service is expressed as amount vs time – two dimensions, not three. Three dimensional bar charts, pie charts, etc. just distort the data you're trying to accurately convey. For more details on this, and definitely if you're not already familiar, read from the master of data visualization, Professor Edward Tufte. But back to debt service…

With rates this low, how much time and money are you spending running and re-running refunding numbers for your issuer clients and targets? This is an expensive, labor intensive, manual task that is far more accurately, predictably, and cost-effectively done across the department through use of a robust database solution that emails results to the banker, advisor, or issuer.

If you have no idea how much time and money is spent performing these tasks, they likely are costing you way too much. After all, what gets measured gets managed…It's 2010 and time to raise the bar. Public finance software has remained substantially unchanged for over a decade, and probably more like two. In this day and age your public finance software, in addition to all the other stuff it's done since TRA86, must add the following five features:

Lots has been studied and even reported on the decision criteria involved in pulling the trigger on a public finance refunding. When is the right time? What bonds do I choose? What savings target do I use? The old rule of thumb that present value (pv) savings should be at least 3% of refunded par is taking some criticism which I won't repeat here. Suffice it to say it's a threshold originally conceived by bankers and as such, the bar for a "Go" decision is not very high. I personally think it's age discrimination; this calculation does have a good three decades under the belt...