“Everything should be made as simple as possible, but not simpler.” - Albert E

Read More

Yesterday I spoke at a luncheon (many thanks to MAGNY for a great event) where, during Q&A, a number of people commented on how difficult it is for those who grew up doing corporate bonds to try to cross over into muni-land’s veritable Oz. With all the talking trees and flying monkeys, munis can be pretty disorienting. And I’ve seen it happen many times myself; graveyards are indeed littered with the corpses of corporate types who come to munis and just never get it, both on the buy-side and the banker/sell-side. They show up bright-eyed and bushy-tailed talking about “benchmark this” and “OAS that” but ultimately wind up crouched in a corner mumbling something about 5 and 10 year bullets.

In Part 1 (a suggested read if you’re getting to this article first) we proposed 3 questions that determine whether bond option pricing models, in contrast to real-world option models, are appropriate for tax-exempt issuers analyzing their callable bonds:

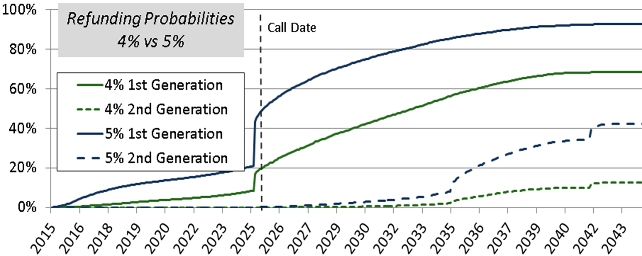

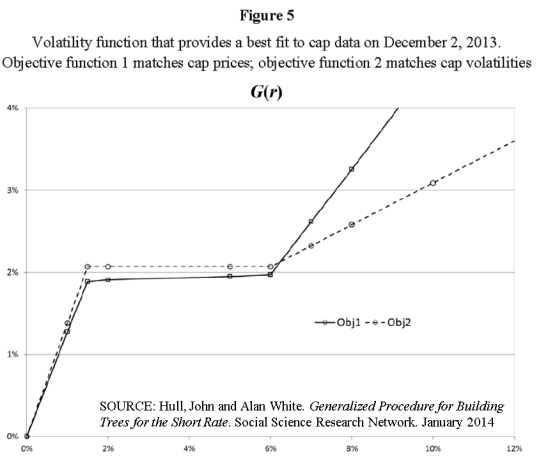

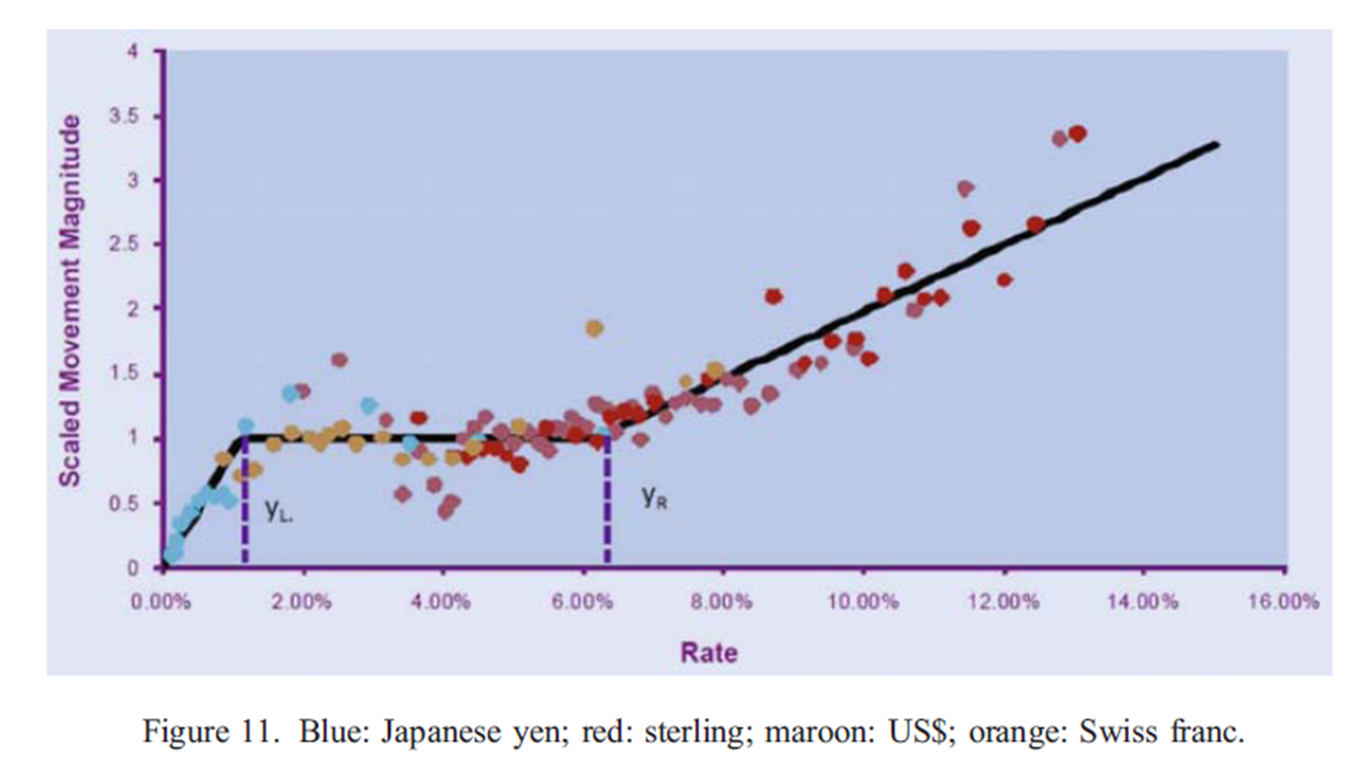

Last summer I wrote an article describing a missing link in rate modeling that had been discovered in exciting new research by Nick Deguillaume, Ricardo Rebonato, and Andry Pogudin entitled The nature of the dependence of the magnitude of rate moves on rates levels: a universal relationship. This mouthful offered two simple takeaways. First, accurately capturing how rates are expected to change, particularly over long time horizons, is central to every rate risk management decision we face. And second, that so-called “standard models” that don’t provide for the observed fact that rates tend to change differently depending on their level aren’t so realistic nor as a result, very good at informing interest rate decisions like refunding opportunities.

"There is no logical way to the discovery of these elemental laws. There is only the way of intuition, which is helped by a feeling for the order lying behind the appearance." - Albert Einstein