Read MoreEssentially, all models are wrong, but some are useful.

- George Box

Read More"I don't think necessity is the mother of invention. Invention, in my opinion, arises directly from idleness, possibly also from laziness - to save oneself trouble."

- Agatha Christie

We see a lot of confusion in public finance as to how to analyze refundings. Unfortunately I think much of it stems from people outside of public finance coming in without a complete understanding of the environment in which a tax-exempt issuer operates i.e. the muni market. These interlopers get excited when they see option specifications in an official statement, then cry out, “We’ve seen these before. We have fantastic models used everywhere else, they must apply here too!” Unfortunately the foundational assumptions underpinning these models do not exist in the muni market leading this statement to be bunk (technical term my father used to use…). In fact those elegant bond options models do not apply in the muni flea market.

"To confuse the model with the world is to embrace a future disaster driven by the belief that humans obey mathematical rules." - The Financial Modeler's Manifesto, Emanual Derman and Paul Wilmott

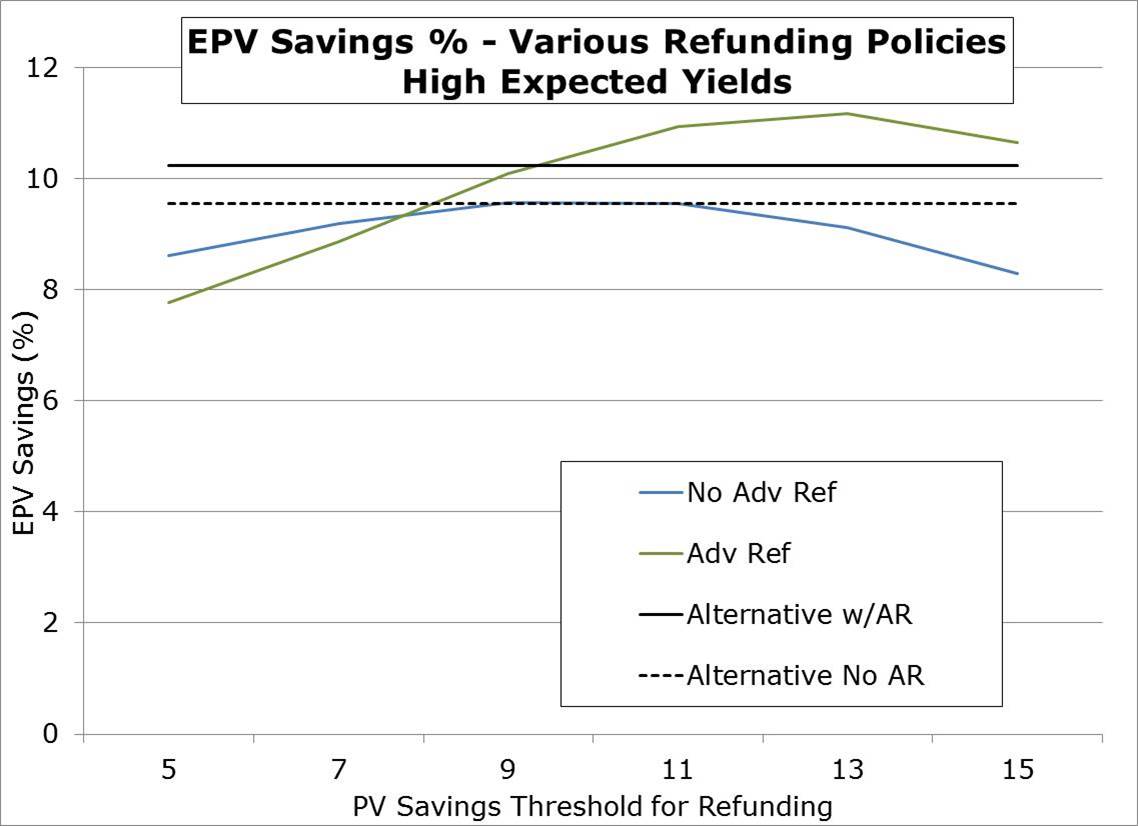

Lots has been studied and even reported on the decision criteria involved in pulling the trigger on a public finance refunding. When is the right time? What bonds do I choose? What savings target do I use? The old rule of thumb that present value (pv) savings should be at least 3% of refunded par is taking some criticism which I won't repeat here. Suffice it to say it's a threshold originally conceived by bankers and as such, the bar for a "Go" decision is not very high. I personally think it's age discrimination; this calculation does have a good three decades under the belt...