"It's not how we make mistakes, but how we correct them, that defines us." - Anonymous

We see a lot of confusion in public finance as to how to analyze refundings. Unfortunately I think much of it stems from people outside of public finance coming in without a complete understanding of the environment in which a tax-exempt issuer operates i.e. the muni market. These interlopers get excited when they see option specifications in an official statement, then cry out, “We’ve seen these before. We have fantastic models used everywhere else, they must apply here too!” Unfortunately the foundational assumptions underpinning these models do not exist in the muni market leading this statement to be bunk (technical term my father used to use…). In fact those elegant bond options models do not apply in the muni flea market.

It’s 2015. Watson vanquished humans in Jeopardy 4 years ago and is now rapidly moving towards replacing as many oncologists as possible. Google is just one company running driverless cars and trucks around everywhere. Facebook is trying to monetize every eye twitch you make looking at a web page. Let’s check in on innovation in public finance:

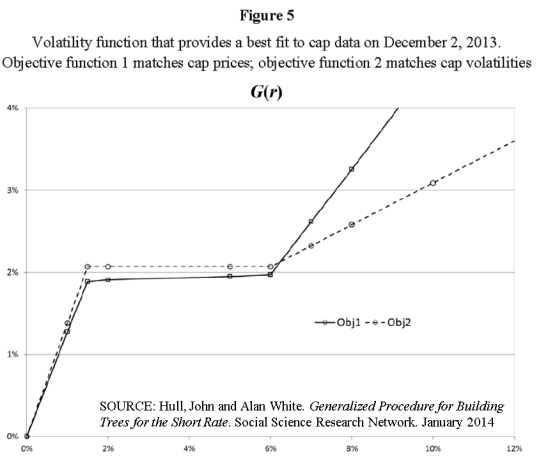

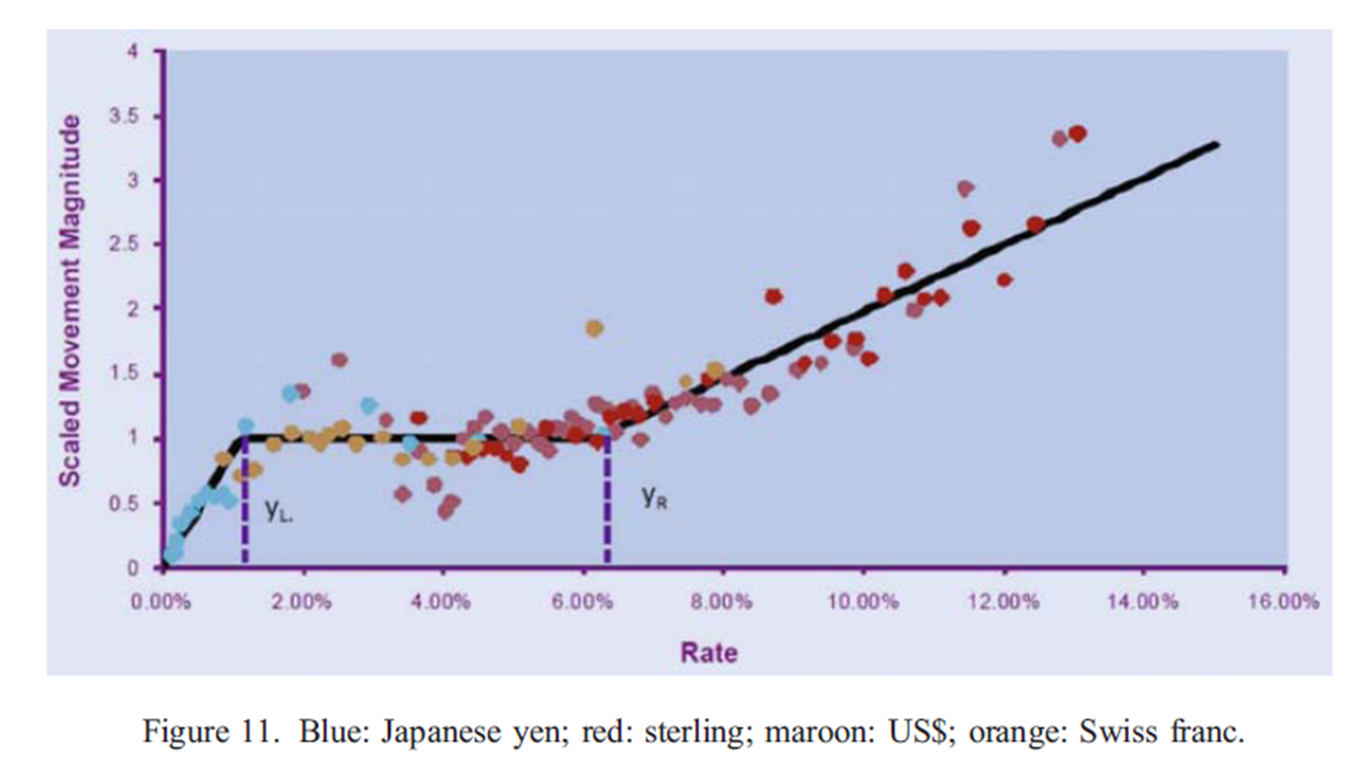

Last summer I wrote an article describing a missing link in rate modeling that had been discovered in exciting new research by Nick Deguillaume, Ricardo Rebonato, and Andry Pogudin entitled The nature of the dependence of the magnitude of rate moves on rates levels: a universal relationship. This mouthful offered two simple takeaways. First, accurately capturing how rates are expected to change, particularly over long time horizons, is central to every rate risk management decision we face. And second, that so-called “standard models” that don’t provide for the observed fact that rates tend to change differently depending on their level aren’t so realistic nor as a result, very good at informing interest rate decisions like refunding opportunities.

"To confuse the model with the world is to embrace a future disaster driven by the belief that humans obey mathematical rules." - The Financial Modeler's Manifesto, Emanual Derman and Paul Wilmott

"There is no logical way to the discovery of these elemental laws. There is only the way of intuition, which is helped by a feeling for the order lying behind the appearance." - Albert Einstein

Today on (Un)Calculated Risk we welcome Shaun Rai, a Managing Director at Montague DeRose and Associates, as our guest contributor (and another outstanding IA client!).

"Despite its role in...finance, the expectations hypothesis (EH) of the term structure of interest rates has received virtually no empirical support." - Predictions of Short-Term Rates and the Expectations Hypothesis, Federal Reserve Bank of St. Louis

If you've taken a break from the news lately, you may have missed the hot water Bloomberg's found themselves in over Bloomberg reporters accessing certain information about Bloomberg users. Finance types scouring for the proverbial free lunch in the markets are understandbly private and the prospect of some Bloomberg journalists looking over their shoulders from those comfy midtown offices is well, unsettling. Of course this is likely overblown by the non-Bloomberg media but we thought the message we got today (below) after logging in to our own Bberg terminal (below) was particularly entertaining and candid...

Topics: Financial Technology, debt profiling, municipal data